Scientists from the London School of Hygiene and Tropical Medicine predict that the infection may peak later this month, but the virus may have infected one in twenty people in Wuhan by the time the peak is reached.

The shortfalls in the comparison made between the SARS virus and Coronavirus and the effect it will have on China as well as the global economy is as follows:

- China currently accounts for 16% of global GDP whereas during the 2002/03 SARS virus it accounted for 4%.

- Global Supply chains are much integrated now than they were in 2002/03.

- There is a greater mobility of people in and out of China, approximately 200,000 per day, which is six times more than in 2002/03.

- Major corporations such as Nike, Disney and Ford have operations in China and their reaction to the coronavirus outbreak, is that it will have an impact not only on operations but on business growth forecasts as shutdowns are enforced.

Analysts from CitiBank, JPMorgan and other investment banks have downgraded China GDP growth from 6.1% to 5.8%. As Wuhan and Hubei province shutdown goes into week three, economies heavily linked to China feel the burn. Australia is already predicting a 0.2 percentage point cut of its economic growth with sectors such as tourism and education severely affected. Analysts have downgraded the Australian Dollar due to natural disasters and the coronavirus in the short term but the 6-month to 1-year outlook remains positive.

Other Asian economies global growth forecast is revised from 4.8% to 4.5, U.S. from 2.3% to 2.2% and Global economy from 3.3% to 3.1%.

Furthermore, when we factor OPEC and its allies considering output cuts by 600,000 barrels per day in light of the shutdown in China to shore up prices as there is less demand for fuel, commodity prices as a whole have suffered.

However, the signing of the phase one U.S. – China trade deal and China cutting tariffs on half of U.S imports and their commitment to increasing purchases of U.S. imports by $100 billion per year over the next two years offers some glimmer of hope.

The speculator:

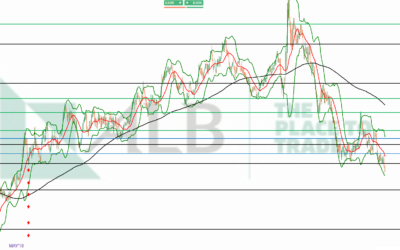

Based on the data we have thus far, I believe the economies most severely impacted may most likely outperform expectation. The Australian Dollar is a perfect example. Price is currently around 0.6675 and hasn’t been at this level since October 2008. 0.6000 has only been reached on five occasions i.e. July 1986, June and August 1998, April 2000, February 2003 and nearly in October 2008. From that level we have seen price rally by 1,000 to 5,000 pips. Price is only 675 pips from this level. Therefore, building a position from current levels all the way to 0.6000 should prices continue to decline could potentially be the trade of the year. Judging by the reports of the coronavirus peaking in the coming weeks, analysts having a positive outlook on the Australian dollar over a one-year horizon, OPEC cutting output to shore up prices, China increasing purchases of U.S. imports and moving into phase two of the trade deal, economies heavily linked to China, should benefit once activity picks up. Downside risk will be the inability to contain the virus and continued shutdown of businesses thereby fuelling even more uncertainty and concern.